Fiancé and I are in the process of joining our finances. For the sake of my own record-keeping and for the benefit of others maybe going through the same thing, I plan to walk through the steps we are taking to meld our financial lives together.

As a reminder, we’ve decided to structure our accounts in a his-hers-ours fashion:

To begin the process of bringing our accounts together, I wanted us to start at the very beginning with the most basic building block of a financial plan.

Yes, that’s right: the dreaded budget.

Steps to create a joint budget

- Draft list of current recurring expenses to personal credit cards and bank accounts.

- Identify which expenses will be considered “joint.”

- Outline a basic budget for the household.

- Agree on rules for joint non-recurring spending and to add new line items to combined budget.

- Check individual credit scores.

Joint versus individual expenses

The first thing we did was lay out all our common expenses and determine whether they would be considered “joint” or “individual.” We agreed that joint expenses would cover those things that are considered “needs” and that are used by us both or pivotal for our general welfare. That means covering the house, the car, health care, groceries, utilities, and basic household and personal care items.

Everything that’s not considered a “need” will be covered by our individual slush funds, which will each get $600/month. This money will not be monitored in our joint Mint account. It’s our own private money that we can do with as we please.

Items that will come out of individual expenses include:

- Shopping

- Entertainment (other than Netflix)

- Takeout/Restaurants

- Fancy gym memberships

- Fancy hair cuts, massages

- Fun individual travel, conferences

- Excessive amounts of eggs

- Pokemon

- Gold-plated waffle iron

The last three items were added by Fiancé. He’s a silly biscuit.

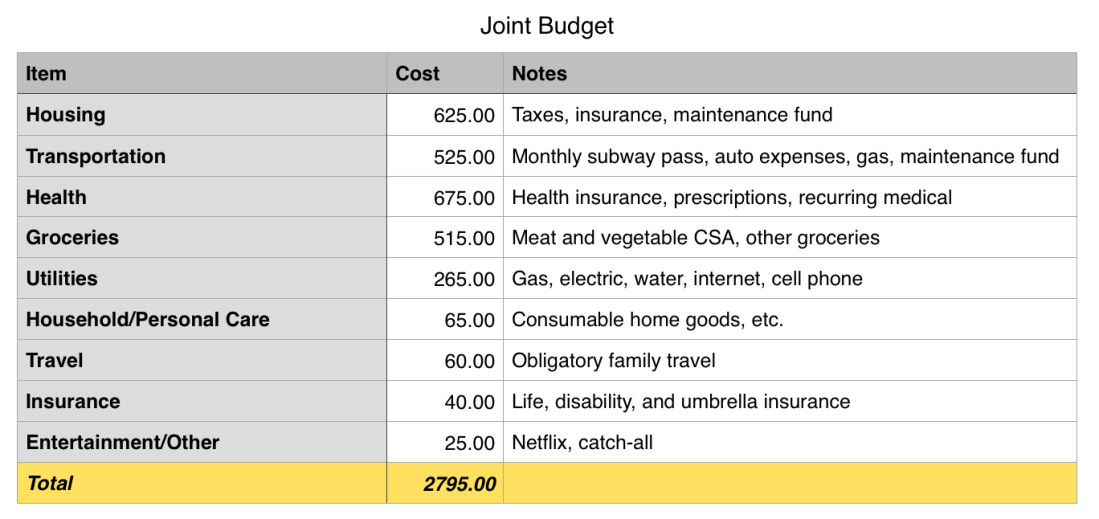

Our household budget

I didn’t realize how much we were spending as a couple until we drafted this combined budget. It was eye-opening and not in a good way.

I’m not going to itemize all our line items, but the below summary by category will give you a good picture of our projected spending. Similar to my monthly updates, this budget does not include mortgage payments or charitable contributions, which are pegged at 10% of our net income.

Right now our joint spending is way higher than I’d like it to be. There are a few clear areas of improvement:

- Once fiancé finds a job that covers his expensive recurring medical costs (which are not being covered by his plan now), we’ll be able to reduce the “Health” category by $400-500.

- Due to a car accident a couple years ago and his new vehicle, fiancé’s car insurance payments are $285 per month, nearly half our monthly transportation budget. I wager we can shop around and knock off $100.

- I’ll also be working to combine our cell phone plans and hopefully cut costs by $25.

If we manage to make progress on these three items, we’ll be able to cut our joint non-mortgage spending down to $2250 per month (the number I’m going to focus on for “Barista FI”). That plus $600 each into our individual spending accounts means we’re expecting a monthly non-mortgage outlay of $3450/month or $41,400/year. Which… isn’t great. But it’s a start. Sigh.

Rules for joint spending

Establishing rules for joint spending will help us make sure we’re not silently inflating our expenses and that we feel comfortable with the level of mutual oversight of our joint money.

We’ve decided that we will:

- Check in with each other when adding new recurring line items, no matter the amount.

- Check in with each other for one-off purchases other than regular household maintenance items.

We plan to set most of our recurring expenses on AutoPay and reconcile our budget quarterly-ish. But still there will be a couple dozen times a month we’ll make joint purchases manually. Since it’d be a hassle to text every time we buy anything jointly, the following items won’t require checking in:

- Auto: Gas, tickets, registration

- Consumable household items — paper towels, toilet paper, etc.

- Consumable personal care — shampoo, soap, lotion, etc.

- Groceries

- Healthcare expenses: minor

This list probably covers 95% of our manual joint spending. For everything else, we’ll give each other notice and have a brief discussion if needed.

Credit scores

Since the next step to combine our finances involves opening checking accounts and credit cards together, I thought we should make it a habit to check in on our joint credit. Luckily for me, in spite of all my churning, I’m still in the high-700s. Fiancé’s score is nearly identical, so we’re in a pretty good spot credit-wise.

Do you and your partner(s) have joint finances? How do you handle individual versus joint spending accounts?

Looks like a pretty good system!

We are 100% joint at this point, but started out with a joint credit card. I don’t remember talking about what was joint and what was individual, but I recall joint was mostly just food and anything we bought at the grocery store and vacation expenses. We split rent unequally (he made much less) to compensate for unequal salary at the time. Then we must have split the credit card 50/50 although I don’t actually remember doing that. I must have paid car expenses until we traded my car for a newer own that was “our car”. Since we were renters, there were fewer household categories. We only lived together 1 year before getting married, and I gradually just took over all the finances.

LikeLike

I think it’s interesting how melding your finances was an incremental, organic progression. Also that you transitioned so quickly to 100% joint. We moved in together about a year into dating and I wasn’t keen on joining our finances at the time. So, four years later, we still have separate accounts (though we’ve been pretty open about finances for the past two years). Since we’re making a big jump, it was important for me to have a *system* that seemed fair and sustainable before introducing it.

LikeLike

Yes, very organic.

I don’t think the 100% joint transition was fast, though. We dated years before moving in together (separate) $, moved in together and married 1 year later (joint CC, but mostly independent management), and after marriage things were still somewhat gradual until he finally finished grad school and there was enough money going into savings that we needed to make larger joint decisions beyond vacations and food. We’ve been married ~8 years and I’d say 100% joint was mostly in the last 4 years.

LikeLike

Ah, that makes sense. I misread and thought you went from living together to married AND joint finances in a year.

LikeLike