Each month I will post an update on my finances to both give you, the reader, some insight into my situation and to give me markers of my progress on my financial journey. My updates consist of two parts:

- Financial Progress Table – Tracks joint net worth progress.

- Spending Table – Compares monthly spending to an average (for us) budget, keeping us accountable for additional expenses. I will also include my personal discretionary budget as well; I will not include my spouse’s discretionary spending, which I do not see.

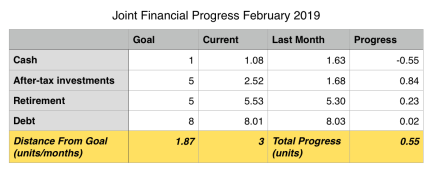

Financial Progress

Each net worth goal in the Financial Progress table is broken down into undisclosed units of money. Our current goal is to reach “Financial Freedom.” By the time we reach this goal we will have:

- A retirement account that can support us when my husband hits 65

- Two college savings funds funded for four years of in-state public university tuition, room, and board

- An emergency fund for six or more months of living expenses

- Sufficient liquidity for my husband and/or I to make a career change with one to two years’ runway

- A mortgage less than two times our combined gross salaries without bonuses or equity.

Once “Financial Freedom” is achieved, the focus will then working be towards “Financial Equilibrium”, where the income from investments covers all our ongoing expenses.

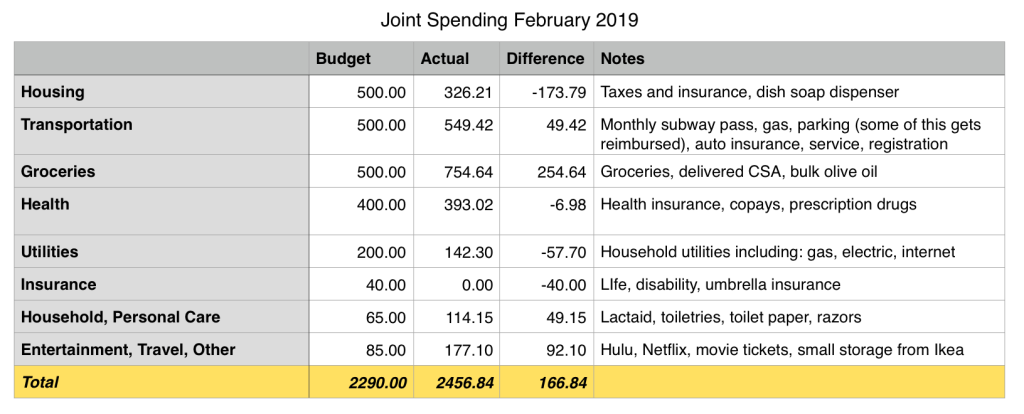

Spending

We’ve created a joint budget which represents the average amount we can expect to spend each month. This is average amount we need to comfortably live in case of a job loss, emergency, etc. I expect to frequently mostly keep in line with our budget when amortized over the year, even though amounts may vary from month to month.

For privacy reasons, there are two things I do not include in our joint spending updates: our monthly mortgage and charitable donations (pegged at 10% of our net income).

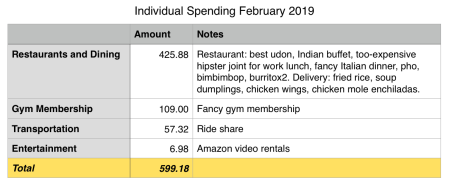

Here is my own personal discretionary spending for the month. I try to spend $600 or less each month for my “fun money” since that’s the allowance that’s apportioned to me and my husband.

Monthly Summary

Life marches on. I’m having trouble being pithy about it.

In any case, I have some financial updates this month.

Good news: got a nice bonus from my employer. I doubt we’re going to see the same level of growth as these past couple months going into the near future, but we should be able to hit our financial inflection point by fall/winter, which is nice.

Bad news: I screwed up our taxes. Or, rather, I over-contributed to my 401(k). Pro tip, the annual $18,500 limit from 2018 is based on total employee contributions per person. I thought it was per plan, which meant I maxed out at my previous employer and at my new one too. Whoops. (But somehow your employer can contribute and you can put in after-tax dollars up to $50-something thousand dollars and that number is per plan? Another LPT: The tax system is broken and for wealthy people.)

At least my over-contributions were Roth dollars, so shouldn’t effect my refund that much. Working now in getting that fixed, but it’s another headache I don’t really feel like I need right now. Plus my husband and I are missing tax forms from our health insurance, which is annoying and necessary for our state returns. Bah, humbug.

Notable things that happened in February include:

- Nothing. 😦

How were your finances in February?

I love your comments on your individual spending, particularly “too expensive hipster joint for work lunch”! It made me laugh. I have a similarly commentary that runs through my head when I review my monthly expenses. Last month was “terrible takeout pizza because I was too lazy to cook”. It helps me evaluate whether expenses were worth it or not and adjust for the next month. I just found your blog and am enjoying reading your posts!

LikeLike

Haha, thanks and welcome!

LikeLike